The licensing framework for Cellular IoT technologies, including NB-IoT, LTE-M, RedCap, and V2X, is quickly becoming unreliable. This is happening because the standardization process itself is evolving rapidly, with each IoT technology entering the market at a different pace and with varying levels of patent involvement.

Multiple factors drive the shift in this Cellular IoT landscape:

- Fragmentation: Unlike earlier standards, where pools provided a more unified licensing approach, the current Cellular IoT ecosystem is split between multiple pools, competing licensing models, and module-level vs. device-level licensing. Each model brings its own set of uncertainties.

- Evolving standardization: Standards like RedCap are still in the innovation phase, with many patents pending, making it hard to predict future royalties or licensing obligations. At the same time, more mature standards like NB-IoT are now entering the enforcement and assertion phases, where companies must address post-deployment claims.

- Patent Declarations vs. Essentiality: Many declarations made during early patent filings for these IoT standards are not truly essential, and as companies rely on these inflated declarations to assess risk, they risk misjudging their exposure.

This misalignment between past practices and the evolving realities of the IoT market may soon put you under unexpected financial pressure, whether through higher royalties, new claims, or unanticipated litigation. This article sheds light on these shifts and reveals how you can navigate the emerging complexities before they become costly problems.

Key Highlights of the Cellular IoT Analysis

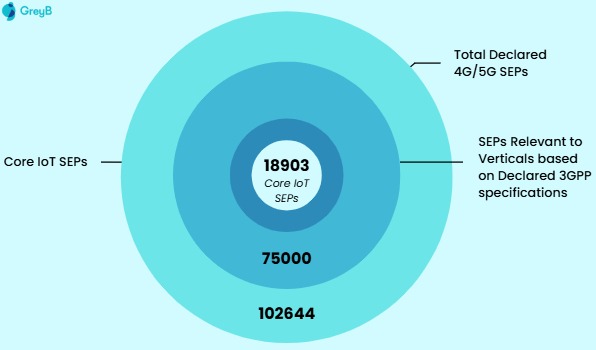

1. A Massive Declaration Fog Masks True Essentiality

The report identifies a striking gap between declared patents and actual relevance. Out of 102,644 declared 4G/5G families, only 18,903 map to IoT-specific technologies such as NB-IoT, LTE-M, RedCap, and V2X.

This means that over 82% of declarations inflate perceived value without meaningfully contributing to IoT implementations.

This early signal indicates that essentiality, not volume, will control future royalty outcomes, mirroring trends seen in Wi-Fi 7 and VVC.

2. Four IoT Technologies, Four Distinct Maturity Curves

NB-IoT and LTE-M show stable, post-peak standards activity, with yearly contributions now focused on refinements rather than new features.

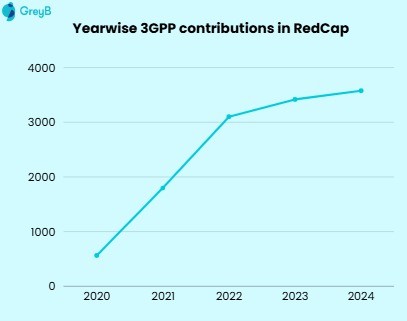

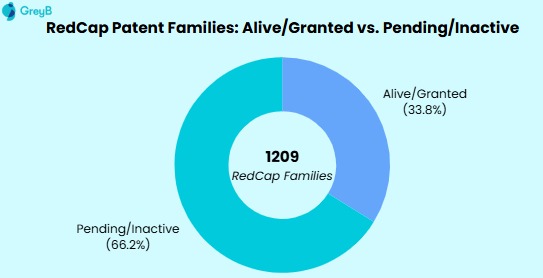

RedCap, by contrast, displays a rapid upward trajectory in 3GPP submissions, with more than 66% of its patents still pending, signaling an early-stage standards race.

Meanwhile, V2X stands apart as the most heavily monetized and mature vertical, yet still with substantial fragmentation outside existing pools. These divergent curves suggest the next phase of licensing disputes will not be uniform; each IoT technology is headed toward a different enforcement and valuation cycle.

3. Influence and Ownership Are Concentrated Among a Small Group

Across NB-IoT, LTE-M, RedCap, and V2X, a consistent group of companies emerges as the dominant forces shaping both technology and standards.

Huawei, Ericsson, Qualcomm, LG, ZTE, Nokia, and now Xiaomi appear repeatedly across patent ownership and Change Request influence, but each plays a different strategic role.

Some companies exert profound architectural influence with fewer patents; others hold large portfolios but limited standards participation. This divergence mirrors historical patterns in wireless and codec standardization, where true power lies in shaping specifications rather than merely filing patents.

4. RedCap Is Becoming the Next Major Licensing Battleground

RedCap’s surging 3GPP contributions, high pending-patent share, and growing interest from both telecom and automotive players mark it as the next significant SEP contest.

Unlike NB-IoT and LTE-M, which are entering monetization phases, RedCap still sits in an active innovation cycle. This positions it in the same “early volatility” category that Wi-Fi 7 and H.267/ECM once occupied, where early contributors will define long-term royalty stakes.

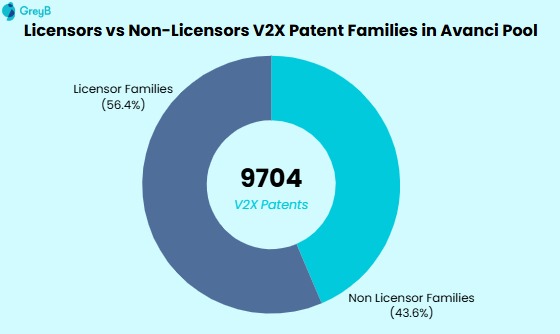

5. V2X Has Consolidated Under Avanci, But With Critical Gaps

While Avanci dominates V2X licensing, covering more than half of all V2X SEP families, over 4,200 families remain outside the pool. This creates an unusual dual exposure for automakers: structured licensing via Avanci, paired with remaining bilateral obligations.

The presence of operators like DTmobile in the top contribution ranks further underscores V2X’s unique blend of telecom and automotive influence.

The Early Signals Reshaping Cellular IoT

The first and most transformative signal comes from the structure of declared SEPs itself. The filtering that reduces 102,644 declared families to 18,903 IoT-relevant SEPs underscores a landscape where strategic clarity cannot rely on declaration volume. Instead, it must be grounded in technical relevance and contribution evidence. The industries preparing for IoT scale, from utilities to automotive, will need this clarity to navigate competing royalty claims and avoid overpaying for irrelevant technologies.

The second signal arises from divergent licensing models. In V2X, Avanci has successfully imposed a unified end-device license for connected vehicles, bringing predictability to automakers but also centralizing power among SEP owners. However, even here, nearly 44% of V2X families remain outside the Avanci pool, creating a dual exposure for OEMs who must secure coverage both within and beyond Avanci. In NB-IoT and LTE-M, Sisvel offers partial consolidation, but again, less than half the landscape sits inside the pool, leaving implementers to negotiate bilaterally for the remainder.

This fragmentation, pools versus component licensors, end-device versus module models, introduces strategic uncertainty that resembles the early licensing cycles of VVC and Wi-Fi 6.

A third defining signal comes from RedCap. Unlike NB-IoT and LTE-M, which peaked in standards activity years ago, RedCap shows sustained year-on-year growth in 3GPP contributions, with companies such as Xiaomi emerging as influential new entrants. With more than 66% of its patent families pending, RedCap is increasingly becoming a future battleground where today’s filings will determine tomorrow’s royalty share. Its importance lies not only in technical evolution but in its ability to serve as the bridge between high-end 5G and low-power IoT, positioning it as the most commercially consequential IoT standard in the medium term.

How Influence and Ownership Are Rebalancing

A distinctive feature of the Cellular IoT landscape is the widening gap between patent ownership and standards influence. Huawei and Ericsson, for example, exercise significant control over the shape of NB-IoT, LTE-M, and V2X through 3GPP Change Requests, even when they do not hold the largest portfolios. Qualcomm maintains a balanced footprint across both layers, blending monetizable assets with meaningful architectural influence. Meanwhile, LG showcases a portfolio-heavy but contribution-light profile, a strategy aligned with long-term royalty extraction rather than forum control.

These varied strategies create an ecosystem where licensing leverage is multidimensional. Those shaping the specifications hold a different kind of power than those having the largest number of granted families. The Cellular IoT licensing cycle will reward organizations that recognize and strategically respond to this distinction.

The Divergent Futures of NB-IoT, LTE-M, RedCap, and V2X

Each technology is heading toward a distinct licensing future.

NB-IoT and LTE-M are now stable, mature standards. Their early innovation peaks have passed, and future activity is likely to focus on enforcement, royalty resets, and strategic assertion by holders who see monetization horizons tightening.

RedCap is on the opposite trajectory. Its ongoing expansion in 3GPP contributions and rising automotive interest position it as the next major SEP battleground. Its valuation will be influenced not only by performance gains but by how its role is interpreted within broader IoT and mid-tier 5G ecosystems.

V2X stands apart as the most monetized and most consolidated IoT standard to date. Avanci’s dominance gives automakers predictable terms, but the significant proportion of non-pool families ensures that V2X licensing is far from settled. With both telecom and automotive players influencing standards, V2X is likely to evolve along a dual-ownership axis rarely seen in wireless standards.

Conclusion

If the current issues are not addressed, licensees will face escalating risks and rising costs due to continued reliance on outdated licensing models. The gap between declaration noise and actual essentiality will only grow. With pool coverage still incomplete, many companies will sign licenses believing they are fully covered, only to find themselves exposed later to new claims from major licensors or competitors.

The Cellular IoT Landscape Report cuts through that uncertainty. By connecting 18,903 IoT-relevant SEPs to multi-year 3GPP activity across the four major standards, it reveals where true influence sits, where gaps remain hidden, and where the next wave of disputes is most likely to emerge. It offers the kind of forward-looking clarity that becomes essential when billions of future devices depend on a still-evolving licensing environment.

In a market this large and this uneven, the advantage shifts to those who understand the changes early and prepare for them before they become pressure points. The report is designed to give you that advantage.